Client General Ledger

Finding the Correct Account Number and other Basic Instructions

By

James Robertson

Table of Contents

1. Account Code Structure

2. Divisions or Business Units

3. Locations or Branches

4. Functions or Departments

5. Matrix

6. Sub-Chart of Accounts per cell

7. Accounts – the main headings

8. Accounts – the second level headings

9. Accounts – the third level headings

10. Accounts – the Master Chart of Accounts

11. Division Specific Accounts

12. Adding Accounts

13. Presentation of the Chart of Accounts

14. Analysis based on the code structure

15. Assistance

16. Appendix – Matrices of Individual Business Units

Client General Ledger

Finding the Correct Account Number and other Basic Instructions

By

James Robertson

The design of the Chart of Accounts is based on work undertaken over more than 23 years with a view to creating logic that allows powerful and flexible consolidation and analysis of financial data.

The Matrix based code element design allows Financials for different business units to be quickly and easily consolidated based on the inherent consolidation rules contained in the code while at the same time allowing the performance of units that carry out the same function to be compared across divisions. This same logic also to allow values of specific accounts to be compared across divisions and business units.

The hierarchical design of all code elements allows data to be rapidly summarized for headline management reporting with drill-down to detail built into the code structure. This facilitates the development of simple but sophisticated reports and models that would otherwise be much more time consuming to create.

The coding conventions of trailing periods and spaces make the codes easy to read and the use of “-“ delimiters is designed for ease of reading and also ease of remembering. Codes are segmented into units of not more than four digits on the basis that such segment lengths are easy to interpret and remember.

The use of Capital Letters for heading accounts, coupled to the use of indents in account descriptions (not in the ERPxxx data but in the Master Chart in the Data Mart) make for quick navigation and ease of reading.

The logic of the Master Chart is designed from the most core (strategic) expenses at the top of the Expense schedule and the least strategic at the bottom. The same logic is used for Revenue.

Assets and Liabilities are structured with least liquid (most long term) at the top and most liquid at the bottom of the list.

Liabilities includes a large block of clearing and control accounts.

Capital and Reserves are situated after Liabilities and followed by Dormant Accounts which are accounts that are no longer active. Some Dormant Accounts are mapped onto the relevant account.

Statistical and Costing data is catered for at the end of the Chart of Accounts.

The overall design is focused on supporting convenient and accurate posting and convenient and accurate strategic and operational analysis of the Financials.

All the data in this document is also contained in a spreadsheet for convenient reference.

1. Account Code structure

The basic design of the Chart of Accounts codes comprises a number of segments:

For example 5-5337-334-99

The form of the code is “Div-LocFunc-Acc1-Acc2”

Where:

Div = the Division code – 1 character, numeric – 5 above

- separator for ease of reading and remembering

Loc = the Location code – 2 character, numeric – 53 above

Func = Function code -- 2 character, numeric – 37 above

- separator

Acc1 = Account Code part 1 – 3 character, numeric or dot “.” – the main categories of Accounts – 334 above

- separator

Acc2 = Account Code part 2 – up to 4 characters, numeric, alpha or blank – the sub-categories of the Accounts – 99 above

2. Divisions or Business Units

The Divisions are the main operating business units of Client:

|

1

|

CLIENT TOWN1

|

ABR

|

|

3

|

CLIENT TOWN2

|

ATwn2

|

|

5

|

CLIENT ALUMINIUM

|

AAL

|

|

7

|

FOUNDRY ENGINEERING CENTRE

|

Division5

|

|

9

|

GROUP HEAD OFFICE

|

GHO

|

Each of these corresponds to a separate ERPxxx Company and Ledger.

In deciding where to post a transaction, first select the ERPxxx Company.

3. Locations or Branches

A Location is a place you can walk to and “kick it” – it is a physical place where you will find people and assets – locations are WHERE we do things.

The Client Locations are:

|

1.

|

TOWN1

|

Brt

|

|

11

|

Factory Town1

|

BFc

|

|

18

|

Admin Building Town1

|

Bad

|

|

19

|

Corporate Office Town1

|

BCO

|

|

1A

|

House1

|

BHD

|

|

3.

|

ROAD1

|

SRd

|

|

31

|

Road1 Plant

|

SMC

|

|

39

|

Admin Building Twn2 Foundry

|

SAB

|

|

5.

|

SUBURB2

|

RSr

|

|

51

|

Plant 1 Aluminium

|

RP1

|

|

53

|

Plant 2 Foundry Aluminium

|

RPF

|

|

54

|

Plant 2 Machining Aluminium

|

RPM

|

|

55

|

Warehouses Aluminium

|

L&D

|

|

57

|

Division5 Plant

|

RFE

|

|

59

|

Admin Building Suburb2

|

Rad

|

|

9.

|

SPECIAL LOCATIONS

|

LSp

|

|

97

|

Function Independent Location

|

LIF

|

|

99

|

Corp Independent Loc & Func

|

LCF

|

In deciding where to post, second select the location code – this is separated from the Division Code by a “-“ so 1-11 is the Town1 Factory.

4. Functions or Departments

A Function is something that People and Assets do – a Function is WHAT we do.

The Client Functions are:

|

0.

|

REVENUE

|

REV

|

|

01

|

Revenue

|

PrT

|

|

1.

|

COST OF SALES

|

REV

|

|

11

|

Cost of Sales

|

PrT

|

|

2.

|

CASTING OPERATIONS

|

CoS

|

|

21

|

Alloying

|

Aly

|

|

22

|

Melting

|

Mlt

|

|

24

|

Sand Plant Operations

|

SPO

|

|

26

|

Core Making

|

CrM

|

|

28

|

Moulding Line

|

Mol

|

|

29

|

Moulding Line 02

|

Mol

|

|

3.

|

FINISHING OPERATIONS

|

FOp

|

|

31

|

Finishing

|

Fin

|

|

33

|

Painting

|

Pnt

|

|

35

|

Heat Treatment

|

HTr

|

|

37

|

Impregnation

|

Imp

|

|

38

|

Welding

|

Wld

|

|

4.

|

MACHINING & ASSEMBLY OPERATIONS

|

MAO

|

|

41

|

Machining

|

Mch

|

|

43

|

Sub-Assembly

|

SAs

|

|

45

|

Final Assembly

|

FAs

|

|

5.

|

OPERATIONAL OVERHEADS

|

OpO

|

|

50

|

Maintenance

|

Mnt

|

|

51

|

Laboratory

|

Lab

|

|

52

|

Inspection Metrology & Q C

|

IMQ

|

|

53

|

Pattern Shop & Tooling Maintenance

|

PST

|

|

54

|

Sand Reclamation

|

SRc

|

|

55

|

Stores

|

Str

|

|

56

|

Logistics and Dispatch

|

L&D

|

|

57

|

Development & Technical

|

Dev

|

|

58

|

Process Engineering

|

PrE

|

|

59

|

Safety Security & Cleaning

|

CSS

|

|

6.

|

TOOLING DESIGN & MANUFACTURE

|

TDM

|

|

65

|

Tool Design & Manufacture

|

TMf

|

|

7.

|

ADMINISTRATION OVERHEADS

|

AdO

|

|

71

|

Administration

|

Adm

|

|

73

|

Sales and Marketing

|

S&M

|

|

75

|

Human Resources

|

Hre

|

|

77

|

IT Function

|

ITF

|

|

9.

|

SPECIAL FUNCTIONS

|

SpF

|

|

98

|

Premises Location Independent Function

|

FIL

|

|

99

|

Corp Independent Location & Function

|

CLF

|

Note that Revenue and Cost of Sales are classified as distinct Functions for convenience of analysis.

In deciding where to post a transaction the third item you will select is the Function.

The Function code is a two digit code immediately following the Location Code so 1-1155 is the Stores at Client Town1 Factory.

Premises or Plant Independent of Function (98) is a function in which items that cannot be allocated to specific functional units are allocated, these are effectively plant wide costs – various items have been allocated to this function depending on preferences of individual business units.

Corporate Independent of Location and Function (99) is a function (and a location) where items that cannot be allocated to specific physical locations and functions are allocated – much of the Financial component of Assets sits here together with most Liabilities

These two elements are designed specifically to cater for the real world complexities of financial data in order to ensure that the final Chart of Accounts models the real world.

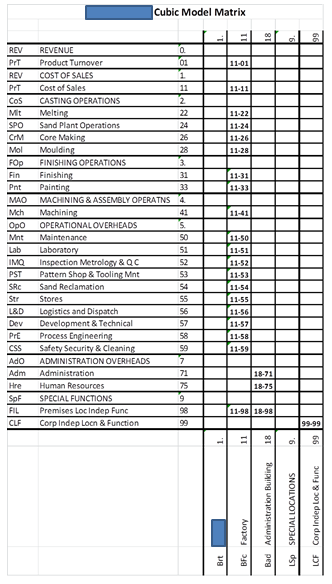

5. Matrix

The Combination of Location and Function produces a Matrix of valid Location-Function intersections which define valid blocks of accounts that model the real world.

The matrix is a logical coding scheme or model designed to make it easy to navigate through the Chart of Accounts both for posting and analysis purposes.

The Chart of Accounts is assembled starting at the top left corner, moving down the column, then from top to bottom down the next column finally ending up in the bottom right corner (9999).

The graphical representation of the matrix below is designed to make it easy for users to find their way around the Chart of Accounts.

The codes in the cells correspond to the Location-Function code pair that describes where in the Chart of Accounts the sub-chart for that cell is to be found.

This is demonstrated by the example below for Division 5:

The Cell number is in the form “Location-Function” – for example 59-71.

In order to determine where to post, once you have selected the Division, select the Location from the list along the bottom of the matrix, you can then see which Functions are present at that Location and select the Function that you want to post to.

You can then select the accounts that apply to that Location-Function intersection or cell.

Note that when you are posting the most convenient approach is to locate the block in the Chart of Accounts that corresponds to the specific cell – that is Location-Function intersection and then simply search that block of accounts, in most cases this will NOT be a long list of accounts and you will quickly find the required account.

If you are looking for a particular account in the Master Chart the following section explains how to do this.

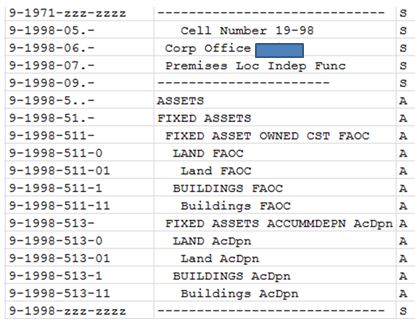

6. Sub-Chart of Accounts per cell

Under each cell in the Matrix is a mini Chart of Accounts which contains ONLY the accounts that apply to that Cell.

This is designed so that a mini-financial statement can be produced for the Manager or Supervisor responsible for each cell.

In the majority of Cells at Client the cell ONLY contains expenses.

Revenue is in separate cells so that the attribution (allocation) of Revenue does not mask the headline expenditure profiles of some business units.

Cost of Sales is separated out for a similar reason.

Following is a very simple example of the Chart of Accounts for Cell 19-98 from the Corporate Office:

Notice the use of zzz-zzzz coupled to a dashed line ----------------------------------- to separate out the blocks of accounts for each cell so that it is easy to navigate the Chart of Accounts. This dashed line is the last possible account code for that Cell.

As a general rule, when writing reports based on account selection the range of accounts should be from the first account in the range to the last possible account in the range (usually contains zeds in place of the trailing blanks of the last possible code sequence before the next account) so that if a new account is added between the limits of the range the report will AUTOMATICALLY be up-to-date. This GREATLY reduces report administration and ensures that complex models and reports remain valid.

At the top of the Chart of Accounts for each cell is the Cell Number which correlates with the Location-Function code in the Account code – this is intended to make the full Chart of Accounts easier to follow.

The next two lines are the Location name and Function name, also for ease of navigation.

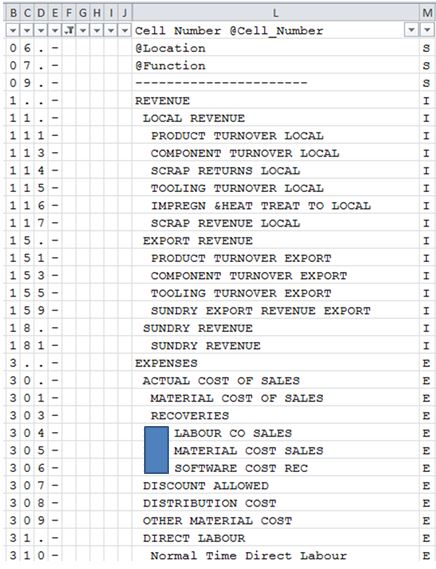

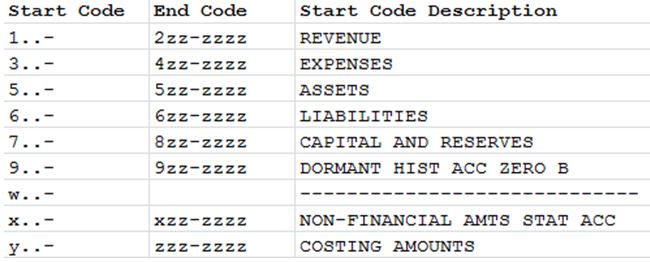

7. Accounts – the main headings

The Master Chart of Accounts is structured hierarchically (cascades) in seven levels starting with the major categories that correspond to the main components of the Balance Sheet and Income Statement.

Note that EXACTLY the same hierarchy and coding applies to the same account no matter which division it occurs in and no matter which cell it occurs in.

This allows you to easily find your way around every division’s Chart of Accounts and also allows you to write reports based on the hierarchies that can easily be used for other divisions.

The hierarchies make it very easy to summarize according to the structure of the code – for example, if you pull a Trial Balance into Excel and split the Account Code into one character segments you can easily use the Filter function to summarize the Trial Balance and give summarized and detailed Income Statements and Balance Sheets.

Following are the main Account headings:

|

1..-

|

REVENUE

|

R

|

|

3..-

|

EXPENSES

|

E

|

|

5..-

|

ASSETS

|

A

|

|

6..-

|

LIABILITIES

|

L

|

|

7..-

|

CAPITAL AND RESERVES

|

C

|

|

9..-

|

DORMANT HISTORICAL ACCOUNTS ZERO BALANCE

|

Varies

|

|

x..-

|

NON-FINANCIAL AMOUNTS STATISTICAL ACCOUNTS

|

S

|

|

y..-

|

COSTING AMOUNTS STATISTICAL ACCOUNTS

|

S

|

Use the above list to select the main category of the transaction that you want to post and then work progressively down the hierarchy.

Notice that the Account logic automatically summarizes into a concise Income Statement and Balance Sheet and by exploding the codes you can produce more and more detailed financial statements. Because of the consistency of coding you can produce more sophisticated analysis than would generally be possible.

If accounts are added it is vital to retain this consistency.

8. Accounts – the second level headings

The next level of accounts is:

|

05.-

|

Cell Number @Cell_Number

|

S

|

|

06.-

|

@Location

|

S

|

|

07.-

|

@Function

|

S

|

|

09.-

|

----------------------

|

S

|

|

1..-

|

REVENUE

|

I

|

|

11.-

|

LOCAL REVENUE

|

I

|

|

15.-

|

EXPORT REVENUE

|

I

|

|

18.-

|

SUNDRY REVENUE

|

I

|

|

3..-

|

EXPENSES

|

E

|

|

30.-

|

ACTUAL COST OF SALES

|

E

|

|

31.-

|

DIRECT LABOUR

|

E

|

|

32.-

|

FIXED FACTORY OVERHEADS

|

E

|

|

33.-

|

VARIABLE FACTORY OVERHEADS

|

E

|

|

34.-

|

ADMIN EXPENSES

|

E

|

|

35.-

|

INTEREST

|

E

|

|

36.-

|

DIVIDENDS

|

E

|

|

37.-

|

EXTRAORDINARY ITEMS

|

E

|

|

38.-

|

TAXATION

|

E

|

|

5..-

|

ASSETS

|

A

|

|

51.-

|

FIXED ASSETS

|

A

|

|

55.-

|

CURRENT ASSETS

|

A

|

|

6..-

|

LIABILITIES

|

L

|

|

61.-

|

NON-CURRENT LIABILITIES

|

L

|

|

65.-

|

CURRENT LIABILITIES

|

L

|

|

7..-

|

CAPITAL AND RESERVES

|

R

|

|

71.-

|

CAPITAL AND RESERVES

|

R

|

|

9..-

|

DORMANT HIST ACC ZERO B

|

L

|

|

99.-

|

DORMANT HIST ACC ZERO BAL

|

L

|

|

w..-

|

-----------------------------

|

S

|

|

x..-

|

NON-FINANCIAL AMTS STAT ACC

|

S

|

|

x1.-

|

NON-FINANCIAL AMOUNTS

|

S

|

|

y..-

|

COSTING AMOUNTS

|

S

|

|

y1.-

|

COSTING AMOUNTS

|

S

|

Notice that the number of digits in the code corresponds to the number of levels of indent.

The indent is provided to make it easy to read the list and find the required item by drilling down the hierarchy.

The corresponding length of the code also makes it easy to follow the hierarchy – each level of hierarchy represents a heading for the levels below so the correct way to read the Chart of Accounts is to follow the cascade of headings until you get to the correct account.

Once you have selected a particular heading drill down to the next level of hierarchy.

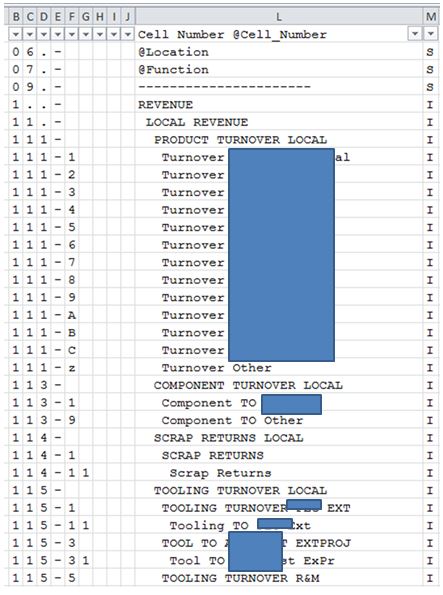

9. Accounts – the third level headings

The third level of accounts is:

|

05.-

|

Cell Number @Cell_Number

|

S

|

|

06.-

|

@Location

|

S

|

|

07.-

|

@Function

|

S

|

|

09.-

|

----------------------

|

S

|

|

1..-

|

REVENUE

|

I

|

|

11.-

|

LOCAL REVENUE

|

I

|

|

111-

|

PRODUCT TURNOVER LOCAL

|

I

|

|

113-

|

COMPONENT TURNOVER LOCAL

|

I

|

|

114-

|

SCRAP RETURNS LOCAL

|

I

|

|

115-

|

TOOLING TURNOVER LOCAL

|

I

|

|

116-

|

IMPREGN &HEAT TREAT TO LOCAL

|

I

|

|

117-

|

SCRAP REVENUE LOCAL

|

I

|

|

15.-

|

EXPORT REVENUE

|

I

|

|

151-

|

PRODUCT TURNOVER EXPORT

|

I

|

|

153-

|

COMPONENT TURNOVER EXPORT

|

I

|

|

155-

|

TOOLING TURNOVER EXPORT

|

I

|

|

159-

|

SUNDRY EXPORT REVENUE EXPORT

|

I

|

|

18.-

|

SUNDRY REVENUE

|

I

|

|

181-

|

SUNDRY REVENUE

|

I

|

|

3..-

|

EXPENSES

|

E

|

|

30.-

|

ACTUAL COST OF SALES

|

E

|

|

301-

|

MATERIAL COST OF SALES

|

E

|

|

303-

|

RECOVERIES

|

E

|

|

304-

|

Division5 LABOUR CO SALES

|

E

|

|

305-

|

Division5 MATERIAL COST SALES

|

E

|

|

306-

|

Division5 SOFTWARE COST REC

|

E

|

|

307-

|

DISCOUNT ALLOWED

|

E

|

|

308-

|

DISTRIBUTION COST

|

E

|

|

309-

|

OTHER MATERIAL COST

|

E

|

|

31.-

|

DIRECT LABOUR

|

E

|

|

310-

|

Normal Time Direct Labour

|

E

|

|

311-

|

Overtime Direct Labour

|

E

|

|

312-

|

Sick Pay Direct Labour

|

E

|

|

313-

|

Allowances Direct Labour

|

E

|

|

314-

|

Bonus & Long Serv Dir Lab

|

E

|

|

315-

|

Company Contrib Dir Labr

|

E

|

|

316-

|

Employee Transport Dir Lab

|

E

|

|

317-

|

Training Direct Labour

|

E

|

|

318-

|

Employee Benefits Dir Labr

|

E

|

|

319-

|

Retrenchment Costs Dir Labr

|

E

|

|

32.-

|

FIXED FACTORY OVERHEADS

|

E

|

|

320-

|

ENERGY

|

E

|

|

321-

|

ENERGY SAVING PROJECTS

|

E

|

|

322-

|

DEPRN FIXED ASSETS (Depn)

|

E

|

|

323-

|

INDIRECT LABOUR

|

E

|

|

324-

|

FIXED REPAIRS &MAINTENANCE

|

E

|

|

325-

|

QUALITY

|

E

|

|

326-

|

PLANT RENTAL

|

E

|

|

327-

|

HEALTH & SAFETY

|

E

|

|

328-

|

INSURANCE

|

E

|

|

329-

|

SUNDRY FIXED FACTORY OH

|

E

|

|

32A-

|

IMPAIRMENT FIX ASSETS (IFA)

|

E

|

|

32B-

|

CANTEEN COSTS

|

E

|

|

33.-

|

VARIABLE FACTORY OVERHEADS

|

E

|

|

331-

|

SCRAP COSTS

|

E

|

|

332-

|

ENERGY & UTILITIES

|

E

|

|

333-

|

VARIABLE REP & MAINT (R&M)

|

E

|

|

334-

|

CONSUMABLES

|

E

|

|

335-

|

TRANSPORT & PACKING

|

E

|

|

336-

|

WASTE REMOVAL & CLEANING

|

E

|

|

338-

|

Division5 LABOUR RECOVERY

|

E

|

|

339-

|

OTHER VARIABLE COSTS

|

E

|

|

34.-

|

ADMIN EXPENSES

|

E

|

|

340-

|

ADMIN STAFF COSTS

|

E

|

|

341-

|

TRAVEL & ACCOMMODATION

|

E

|

|

342-

|

ASSET RELATED ADMIN COSTS

|

E

|

|

343-

|

FEES PAID TO THIRD PARTIES

|

E

|

|

344-

|

ADMIN VEHICLE EXPENSES

|

E

|

|

345-

|

GENERAL ADMIN EXPENSES

|

E

|

|

346-

|

COMPUTER & COMMN COSTS

|

E

|

|

349-

|

SUNDRY ADMIN EXPENSES

|

E

|

|

35.-

|

INTEREST

|

E

|

|

351-

|

INTEREST

|

E

|

|

36.-

|

DIVIDENDS

|

E

|

|

361-

|

DIVIDENDS

|

E

|

|

37.-

|

EXTRAORDINARY ITEMS

|

E

|

|

371-

|

EXTRAORDINARY ITEMS

|

E

|

|

38.-

|

TAXATION

|

E

|

|

381-

|

TAXATION

|

E

|

|

5..-

|

ASSETS

|

A

|

|

51.-

|

FIXED ASSETS

|

A

|

|

511-

|

FIXED ASSET OWNED CST FAOC

|

A

|

|

513-

|

FIXED ASSETS ACC DEPN AcDpn

|

A

|

|

55.-

|

CURRENT ASSETS

|

A

|

|

551-

|

INVENTORY

|

A

|

|

553-

|

TRADE DEBTORS

|

A

|

|

558-

|

OTHER DEBTORS

|

A

|

|

559-

|

BANK & CASH

|

A

|

|

6..-

|

LIABILITIES

|

L

|

|

61.-

|

NON-CURRENT LIABILITIES

|

L

|

|

611-

|

LONG TERM LOANS

|

L

|

|

613-

|

FINANCE LEASES

|

L

|

|

615-

|

xxx NOT REQUIRED

|

L

|

|

619-

|

OTH NON-CURRENT LIAB

|

L

|

|

65.-

|

CURRENT LIABILITIES

|

L

|

|

650-

|

ACCOUNTS PAYABLE

|

L

|

|

651-

|

CLEARING ACCOUNTS

|

L

|

|

652-

|

CURRENT LOANS

|

L

|

|

654-

|

FINANCE LEASES

|

L

|

|

656-

|

CALL ACCOUNTS

|

L

|

|

657-

|

TAX PAYABLE

|

L

|

|

658-

|

DIVIDENDS PAYABLE

|

L

|

|

659-

|

OTHER CURRENT LIABILITIES

|

L

|

|

7..-

|

CAPITAL AND RESERVES

|

R

|

|

71.-

|

CAPITAL AND RESERVES

|

R

|

|

711-

|

SHARE CAPITAL

|

R

|

|

713-

|

SHARE PREMIUM

|

R

|

|

715-

|

EQUITY LOANS

|

R

|

|

717-

|

NON-DISTRIBUTABLE RESERVES

|

R

|

|

719-

|

RETAINED EARNINGS ACCUM DEF

|

R

|

|

9..-

|

DORMANT HIST ACC ZERO B

|

L

|

|

99.-

|

DORMANT HIST ACC ZERO BAL

|

L

|

|

999-

|

DORMANT HIST ACC ZERO BAL

|

L

|

|

w..-

|

-----------------------------

|

S

|

|

x..-

|

NON-FINANCIAL AMTS STAT ACC

|

S

|

|

x1.-

|

NON-FINANCIAL AMOUNTS

|

S

|

|

x11-

|

STATISTICAL VALUES

|

S

|

|

y..-

|

COSTING AMOUNTS

|

S

|

|

y1.-

|

COSTING AMOUNTS

|

S

|

|

y18-

|

COSTING AMOUNTS

|

S

|

Notice that headings are in capital letters and posting level accounts are in proper case – this is also intended to make it easier to navigate the Chart of Accounts.

In general ONLY budgets should be posted against headings, transactions should all be posted against the proper case posting level accounts.

10. Accounts – the Master Chart of Accounts

Once you have drilled down to this level you will be very close to the required account and you can search in the main Chart of Accounts as follows:

|

05.-

|

Cell Number @Cell_Number

|

S

|

|

06.-

|

@Location

|

S

|

|

07.-

|

@Function

|

S

|

|

09.-

|

----------------------

|

S

|

|

1..-

|

REVENUE

|

I

|

|

11.-

|

LOCAL REVENUE

|

I

|

|

111-

|

PRODUCT TURNOVER LOCAL

|

I

|

|

111-1

|

Turnover Customer1

|

I

|

|

111-2

|

Turnover Customer2

|

I

|

|

111-3

|

Turnover Customer3

|

I

|

|

111-4

|

Turnover Customer4

|

I

|

|

111-5

|

Turnover Customer5

|

I

|

|

111-6

|

Turnover Customer6

|

I

|

|

111-7

|

Turnover Customer7

|

I

|

|

111-8

|

Turnover Customer8

|

I

|

|

111-9

|

Turnover Customer9

|

I

|

|

111-A

|

Turnover Customer10

|

I

|

|

111-B

|

Turnover Customer11

|

I

|

|

111-C

|

Turnover Customer12

|

I

|

|

111-z

|

Turnover Other

|

I

|

|

113-

|

COMPONENT TURNOVER LOCAL

|

I

|

|

113-1

|

Component TO Customer12

|

I

|

|

113-9

|

Component TO Other

|

I

|

|

114-

|

SCRAP RETURNS LOCAL

|

I

|

|

114-1

|

SCRAP RETURNS

|

I

|

|

114-11

|

Scrap Returns

|

I

|

|

115-

|

TOOLING TURNOVER LOCAL

|

I

|

|

115-1

|

TOOLING TURNOVER Division5 EXT

|

I

|

|

115-11

|

Tooling TO Division5 Ext

|

I

|

|

115-3

|

TOOL TO CLIENT EXTPROJ

|

I

|

|

115-31

|

Tool TO Client ExPr

|

I

|

|

115-5

|

TOOLING TURNOVER R&M

|

I

|

|

115-51

|

Tooling TO R&M Town1

|

I

|

|

115-53

|

Tooling TO R&M Twn2

|

I

|

|

115-54

|

Tooling TO R&M Alu

|

I

|

|

115-55

|

Tooling TO R&M Division5

|

I

|

|

115-8

|

TOOLING REPLACEMENT TO

|

I

|

|

115-81

|

Tool Repl TO Town1

|

I

|

|

115-83

|

Tool Repl TO Twn2

|

I

|

|

115-84

|

Tool Repl TO Alu

|

I

|

|

115-85

|

Tool Repl TO Division5

|

I

|

|

115-9

|

TOOLING OTHER

|

I

|

|

115-91

|

Tooling Other

|

I

|

|

116-

|

IMPREGN &HEAT TREAT TO LOCAL

|

I

|

|

116-1

|

Impregnation Turnover

|

I

|

|

116-5

|

Heat Treatment Turnover

|

I

|

|

117-

|

SCRAP REVENUE LOCAL

|

I

|

|

117-1

|

SALES OF SCRAP IRON

|

I

|

|

117-11

|

Swarf

|

I

|

|

117-15

|

Other Scrap Iron

|

I

|

|

117-5

|

SALES OF SCRAP ALUMINIUM

|

I

|

|

117-51

|

Sales Scrap Aluminium

|

I

|

|

15.-

|

EXPORT REVENUE

|

I

|

|

151-

|

PRODUCT TURNOVER EXPORT

|

I

|

|

151-1

|

Turnover Customer13

|

I

|

|

151-5

|

Turnover Customer14

|

I

|

|

151-7

|

Turnover Customer15

|

I

|

|

151-9

|

Turnover Other

|

I

|

|

153-

|

COMPONENT TURNOVER EXPORT

|

I

|

|

153-1

|

Component Turnover

|

I

|

|

155-

|

TOOLING TURNOVER EXPORT

|

I

|

|

155-1

|

Turnover Customer15

|

I

|

|

155-9

|

Turnover Other

|

I

|

|

159-

|

SUNDRY EXPORT REVENUE EXPORT

|

I

|

|

159-1

|

EXPORT INCENTIVES

|

I

|

|

159-11

|

APDP Incentives

|

I

|

|

159-15

|

MIDP Incentives

|

I

|

|

159-9

|

OTH SUNDRY EXPORT REVENUE

|

I

|

|

159-99

|

Oth Sundry Export Rev

|

I

|

|

18.-

|

SUNDRY REVENUE

|

I

|

|

181-

|

SUNDRY REVENUE

|

I

|

|

181-1

|

PR ORLOSS CUSTMR TOOL PR

|

I

|

|

181-11

|

Pr Loss Custmr Tool Pr

|

I

|

|

181-2

|

AIS & EIP BENEFITS

|

I

|

|

181-21

|

AIS Benefits

|

I

|

|

181-25

|

EIP Benefits

|

I

|

|

181-3

|

SETTLEMENT DISC RECEIVED

|

I

|

|

181-31

|

Settlement Disc Recd

|

I

|

|

181-4

|

TRAINING REBATES

|

I

|

|

181-41

|

MERSETA Rebates

|

I

|

|

181-49

|

Other Training Rebates

|

I

|

|

181-5

|

PR OR LOSS SALE FIX ASST

|

I

|

|

181-51

|

Pr or Loss Sale Fix Ass

|

I

|

|

181-6

|

PROFIT ON FOREX

|

I

|

|

181-61

|

Profit on Forex

|

I

|

|

181-7

|

DIVIDENDS RECEIVED

|

I

|

|

181-71

|

Dividends Received

|

I

|

|

181-8

|

SUNDRY INTERNAL SALES

|

I

|

|

181-81

|

Sundry Internal Sales

|

I

|

|

181-9

|

OTHER SUNDRY REVENUE

|

I

|

|

181-99

|

Other Sundry Revenue

|

I

|

|

3..-

|

EXPENSES

|

E

|

|

30.-

|

ACTUAL COST OF SALES

|

E

|

|

301-

|

MATERIAL COST OF SALES

|

E

|

|

301-1

|

CLIENT BANK COST OF SALES

|

E

|

|

301-11

|

Standard Cost of Sales

|

E

|

|

301-13

|

Profit Scrap Alloying

|

E

|

|

301-5

|

VARIANCES

|

E

|

|

301-51

|

MATL USAGE VARIANCE

|

E

|

|

301-510

|

CAST IRON MELTING USE VAR

|

E

|

|

301-5100

|

Scrap steel Use Var

|

E

|

|

301-5101

|

Pig Iron Use Var

|

E

|

|

301-5102

|

Copper Use Var

|

E

|

|

301-5103

|

Tin Use Var

|

E

|

|

301-5104

|

Silicon Carbide Use Var

|

E

|

|

301-5105

|

Silicon Use Var

|

E

|

|

301-5106

|

Manganese Use Var

|

E

|

|

301-5107

|

Molybdenum Use Var

|

E

|

|

301-5109

|

Oth Cast Iron Comp UseVr

|

E

|

|

301-511

|

ALUMINIUM MELTING USE VAR

|

E

|

|

301-5111

|

Alum Ingot Ford Use Var

|

E

|

|

301-5112

|

Alum Ingot EA111 Use Var

|

E

|

|

301-5114

|

Gas Use Var

|

E

|

|

301-5119

|

Oth Alum Components UseV

|

E

|

|

301-512

|

CORE MAKING USE VAR

|

E

|

|

301-5121

|

Sand Use Var

|

E

|

|

301-5123

|

Core Making Resins UseVr

|

E

|

|

301-5125

|

Gas Use Var

|

E

|

|

301-513

|

MOULDING & CASTING USE VR

|

E

|

|

301-5131

|

Magnesium Use Var

|

E

|

|

301-5133

|

ME85 Innoculant Use Var

|

E

|

|

301-5135

|

Filters Use Var

|

E

|

|

301-5139

|

Other Moulding Use Var

|

E

|

|

301-514

|

POWDER COATING USE VAR

|

E

|

|

301-5141

|

Powder Coat Matls Use Vr

|

E

|

|

301-515

|

FINISHING & FETLING USE V

|

E

|

|

301-5151

|

Fin & Fetling Matls UseV

|

E

|

|

301-516

|

IMPREGNATION USE VAR

|

E

|

|

301-5161

|

Impregnation Resins UseV

|

E

|

|

301-517

|

MACHINING USE VAR

|

E

|

|

301-5171

|

Cut Fld & Hydr Oils UseV

|

E

|

|

301-518

|

ASSEMBLY USE VAR

|

E

|

|

301-5181

|

Subcomponents Use Var

|

E

|

|

301-519

|

OTH MATL USE VARIANCE

|

E

|

|

301-5191

|

Oth Matl U Var CASTING

|

E

|

|

301-5192

|

Oth Matl U Var Alloying

|

E

|

|

301-5193

|

Oth Matl U Var Melting

|

E

|

|

301-5194

|

Oth Matl U Var Sand Plt

|

E

|

|

301-5195

|

Oth Matl U Var Core Makg

|

E

|

|

301-5196

|

Oth Matl U Var Moulding1

|

E

|

|

301-5197

|

Oth Matl U Var Moulding2

|

E

|

|

301-5198

|

Oth Matl U Var FINISH

|

E

|

|

301-5199

|

Oth Matl U Var Finishing

|

E

|

|

301-519A

|

Oth Matl U Var Painting

|

E

|

|

301-519B

|

Oth Matl U Var Heat Trt

|

E

|

|

301-519C

|

Oth Matl U Var Impregn

|

E

|

|

301-519D

|

Oth Matl U Var Welding

|

E

|

|

301-519E

|

Oth Matl U Var MCH&ASSBL

|

E

|

|

301-519F

|

Oth Matl U Var Machng

|

E

|

|

301-519G

|

Oth Matl U Var SubAssbly

|

E

|

|

301-519H

|

Oth Matl U Var FinalAssb

|

E

|

|

301-519I

|

Oth Matl U Var OPERN OH

|

E

|

|

301-519J

|

Oth Matl U Var Maint

|

E

|

|

301-519K

|

Oth Matl U Var Lab

|

E

|

|

301-519L

|

Oth Matl U Var InsMet QC

|

E

|

|

301-519M

|

Oth Matl U Var PatShp&Tl

|

E

|

|

301-519N

|

Oth Matl U Var Sand Recl

|

E

|

|

301-519O

|

Oth Matl U Var Stores

|

E

|

|

301-519P

|

Oth Matl U Var Log &Disp

|

E

|

|

301-519Q

|

Oth Matl U Var Dev &Tech

|

E

|

|

301-519R

|

Oth Matl U Var Proc Eng

|

E

|

|

301-519S

|

Oth Matl U Var SafSecCln

|

E

|

|

301-519T

|

Oth M U Var TOOL DES MAN

|

E

|

|

301-519U

|

Oth M U Var Tool Des Man

|

E

|

|

301-519V

|

Oth Matl U Var ADMIN OH

|

E

|

|

301-519W

|

Oth Matl U Var Admin

|

E

|

|

301-519X

|

Oth Matl U Var Sale &Mkt

|

E

|

|

301-519Y

|

Oth Matl U Var HR

|

E

|

|

301-519Z

|

Oth Matl U Var IT

|

E

|

|

301-53

|

PURCHASE PRICE VARIANCE

|

E

|

|

301-531

|

Purch Price Variance

|

E

|

|

301-55

|

OPER MATLS PRICE VAR

|

E

|

|

301-551

|

Op Matls Price Var

|

E

|

|

301-57

|

STOCK REVALUATION

|

E

|

|

301-571

|

Stock Revaluation

|

E

|

|

301-58

|

STOCK LOSSES (GAINS)

|

E

|

|

301-581

|

Stock Losses (Gains)

|

E

|

|

303-

|

RECOVERIES

|

E

|

|

303-1

|

DIRECT LABOUR RECOVER

|

E

|

|

303-11

|

Direct Labour Recover

|

E

|

|

303-12

|

FOUNDRY OP DIR LAB REC

|

E

|

|

303-121

|

Alloying Dir Lab Rec

|

E

|

|

303-122

|

Melting Dir Lab Rec

|

E

|

|

303-124

|

Sand Plant Ops DirLabRec

|

E

|

|

303-126

|

Core Making Dir Lab Rec

|

E

|

|

303-128

|

Moulding Dir Lab Rec

|

E

|

|

303-13

|

FINISHING OPS DIR LAB REC

|

E

|

|

303-131

|

Finishing Dir Lab Rec

|

E

|

|

303-133

|

Painting Dir Lab Rec

|

E

|

|

303-135

|

Heat Treat Dir Lab Rec

|

E

|

|

303-137

|

Impregnation Dir Lab Rec

|

E

|

|

303-138

|

Welding Dir Lab Rec

|

E

|

|

303-14

|

MACH &ASSM OPS DIR LAB REC

|

E

|

|

303-141

|

Machining Dir Lab Rec

|

E

|

|

303-143

|

Sub-Assembly Dir Lab Rec

|

E

|

|

303-145

|

Final Assm Dir Lab Rec

|

E

|

|

303-19

|

OTH DIR LABOUR RECVD

|

E

|

|

303-199

|

Oth Dir Labr Recvd

|

E

|

|

303-3

|

FIX FACT OH RECOVERY

|

E

|

|

303-31

|

Fixed Fact OH Recov

|

E

|

|

303-32

|

FOUNDRY OPS FIX FACT OH

|

E

|

|

303-321

|

Alloying Fix Fact OH

|

E

|

|

303-322

|

Melting Fix Fact OH

|

E

|

|

303-324

|

Sand Plt Ops Fix Fact OH

|

E

|

|

303-326

|

Core Making Fix Fact OH

|

E

|

|

303-328

|

Moulding Fix Fact OH

|

E

|

|

303-33

|

FINISHING OPS FIX FACT OH

|

E

|

|

303-331

|

Finishing Fix Fact OH

|

E

|

|

303-333

|

Painting Fix Fact OH

|

E

|

|

303-335

|

Heat Treat Fix Fact OH

|

E

|

|

303-337

|

Impregnation Fix Fact OH

|

E

|

|

303-338

|

Welding Fix Fact OH

|

E

|

|

303-34

|

MACH &ASSB OPS FIX FACT OH

|

E

|

|

303-341

|

Machining Fix Fact OH

|

E

|

|

303-343

|

Sub-Assembly Fix Fact OH

|

E

|

|

303-345

|

Final Assem Fix Fact OH

|

E

|

|

303-39

|

OTH DIR LABOUR RECD

|

E

|

|

303-399

|

Oth Dir Labr Recvd

|

E

|

|

303-5

|

VAR FACT OH RECOVERY

|

E

|

|

303-51

|

Var Fact OH Recovery

|

E

|

|

303-52

|

FOUNDRY OPS VAR FACT OH

|

E

|

|

303-521

|

Alloying Var Fact OH

|

E

|

|

303-522

|

Melting Var Fact OH

|

E

|

|

303-524

|

Sand Plt Ops Var Fact OH

|

E

|

|

303-526

|

Core Making Var Fact OH

|

E

|

|

303-528

|

Moulding Var Fact OH

|

E

|

|

303-53

|

FINISHING OPS VAR FACT OH

|

E

|

|

303-531

|

Finishing Var Fact OH

|

E

|

|

303-533

|

Painting Var Fact OH

|

E

|

|

303-535

|

Heat Treat Var Fact OH

|

E

|

|

303-537

|

Impregnation Var Fact OH

|

E

|

|

303-538

|

Welding Var Fact OH

|

E

|

|

303-54

|

MACH &ASSM OPS VAR FACT OH

|

E

|

|

303-541

|

Machining Var Fact OH

|

E

|

|

303-543

|

Sub-Assembly Var Fact OH

|

E

|

|

303-545

|

Final Assem Var Fact OH

|

E

|

|

303-59

|

OTH DIR LABOUR RECD

|

E

|

|

303-599

|

Oth Dir Labour Recd

|

E

|

|

303-7

|

SUBCONTRACTOR RECOVERY

|

E

|

|

303-71

|

Subcontractor Revy

|

E

|

|

304-

|

Division5 LABOUR CO SALES

|

E

|

|

304-1

|

Division5 Labour Cost Sales

|

E

|

|

305-

|

Division5 MATERIAL COST SALES

|

E

|

|

305-1

|

Division5 Material Cost of Sales

|

E

|

|

306-

|

Division5 SOFTWARE COST REC

|

E

|

|

306-1

|

Magmasoft Recoveries

|

E

|

|

307-

|

DISCOUNT ALLOWED

|

E

|

|

307-1

|

Discount Allowed

|

E

|

|

308-

|

DISTRIBUTION COST

|

E

|

|

308-1

|

FOB Costs

|

E

|

|

308-3

|

Post FOB Costs

|

E

|

|

308-5

|

Shipping Insurance

|

E

|

|

309-

|

OTHER MATERIAL COST

|

E

|

|

309-9

|

Other Material Cost

|

E

|

|

31.-

|

DIRECT LABOUR

|

E

|

|

310-

|

Normal Time Direct Labour

|

E

|

|

310-1

|

Normal Time Direct Labr

|

E

|

|

310-5

|

Contract Wrkr Dir Labour

|

E

|

|

311-

|

Overtime Direct Labour

|

E

|

|

312-

|

Sick Pay Direct Labour

|

E

|

|

313-

|

Allowances Direct Labour

|

E

|

|

314-

|

Bonus & Long Serv Dir Lab

|

E

|

|

314-1

|

Bonus Direct Labour

|

E

|

|

314-3

|

Gainshare Pay Dir Labour

|

E

|

|

314-7

|

Long Service Awd Dir Lab

|

E

|

|

314-8

|

Year-End Vouch Dir Lab

|

E

|

|

315-

|

Company Contrib Dir Labr

|

E

|

|

315-1

|

Leave Pay Direct Labour

|

E

|

|

315-2

|

Year End Bonus Dir Labr

|

E

|

|

315-3

|

Pension Direct Labour

|

E

|

|

315-4

|

Provident Fund Dir Labr

|

E

|

|

315-5

|

Medical Aid Dir Labr

|

E

|

|

315-6

|

UIF Direct Labour

|

E

|

|

315-7

|

Skills Deve Levy Dir Labr

|

E

|

|

315-8

|

Workmans Comp Dir Labr

|

E

|

|

316-

|

Employee Transport Dir Lab

|

E

|

|

317-

|

Training Direct Labour

|

E

|

|

318-

|

Employee Benefits Dir Labr

|

E

|

|

319-

|

Retrenchment Costs Dir Labr

|

E

|

|

32.-

|

FIXED FACTORY OVERHEADS

|

E

|

|

320-

|

ENERGY

|

E

|

|

320-1

|

Electricity -- KVA

|

E

|

|

320-2

|

Gas Tank Rental

|

E

|

|

321-

|

ENERGY SAVING PROJECTS

|

E

|

|

321-1

|

Energy Saving Proj Exp

|

E

|

|

322-

|

DEPRN FIXED ASSETS (Depn)

|

E

|

|

322-0

|

LAND Depn

|

E

|

|

322-1

|

Land Depn

|

E

|

|

322-1

|

BUILDINGS Depn

|

E

|

|

322-11

|

Buildings Depn

|

E

|

|

322-13

|

Leasehold Improvements

|

E

|

|

322-2

|

PLANT & MACHINERY Depn

|

E

|

|

322-21

|

Maint Spares Stock Depn

|

E

|

|

322-29

|

Oth Plt & Machry Depn

|

E

|

|

322-4

|

MOTOR VEHICLES Depn

|

E

|

|

322-41

|

Forklifts Depn

|

E

|

|

322-49

|

Oth Motor Vehicles Depn

|

E

|

|

322-5

|

OFFICE EQUIPMENT Depn

|

E

|

|

322-51

|

Office Equipment Depn

|

E

|

|

322-6

|

COMPUTERS Depn

|

E

|

|

322-61

|

Computers Depn

|

E

|

|

322-7

|

FURNITURE & FITTINGS Depn

|

E

|

|

322-71

|

Furniture & Fitt Depn

|

E

|

|

322-8

|

INTANGIBLE ASSETS Depn

|

E

|

|

322-81

|

Intangible Assets Depn

|

E

|

|

323-

|

INDIRECT LABOUR

|

E

|

|

323-1

|

FACTORY SAL IND LABR

|

E

|

|

323-10

|

Normal Time Ind Labr Sal

|

E

|

|

323-11

|

Overtime Ind Labr Sal

|

E

|

|

323-13

|

Allowances Ind Labr Sal

|

E

|

|

323-15

|

Bonus &Lg Serv Ind Lab Sal

|

E

|

|

323-17

|

Comp Contrib Ind Labr Sal

|

E

|

|

323-18

|

Retrench Costs Ind Lab Sal

|

E

|

|

323-5

|

INDIRECT WAGES

|

E

|

|

323-50

|

Normal Time Ind Wg

|

E

|

|

323-501

|

Normal Time Ind Wg

|

E

|

|

323-505

|

Contract Work Ind Wg

|

E

|

|

323-51

|

Overtime Ind Wg

|

E

|

|

323-52

|

Sick Pay Ind Wg

|

E

|

|

323-53

|

Allowances Ind Wg

|

E

|

|

323-54

|

Bonus Long Serv Ind Wg

|

E

|

|

323-55

|

Company Contrib Ind Wg

|

E

|

|

323-56

|

Employee Trans Ind Wg

|

E

|

|

323-57

|

Training Ind Wg

|

E

|

|

323-58

|

Employee Ben Ind Wg

|

E

|

|

323-59

|

Retrench Costs Ind Wg

|

E

|

|

324-

|

FIXED REPAIRS &MAINTENANCE

|

E

|

|

324-2

|

PLANT & MACHINERY R&M

|

E

|

|

324-21

|

Fix Impr Mach Elect

|

E

|

|

324-22

|

Fix Impr Mach Mech

|

E

|

|

324-25

|

Fixed Shutdown Elec R&M

|

E

|

|

324-26

|

Fixed Shutdown Mech R&M

|

E

|

|

324-29

|

Oth Fix R&M Plt & Mach

|

E

|

|

324-4

|

MOTOR VEHICLES R&M

|

E

|

|

324-41

|

Forklift R&M

|

E

|

|

324-49

|

Oth Motor Veh R&M

|

E

|

|

325-

|

QUALITY

|

E

|

|

325-1

|

Certification Costs

|

E

|

|

325-5

|

Calibration Costs

|

E

|

|

325-8

|

Quality Costs

|

E

|

|

326-

|

PLANT RENTAL

|

E

|

|

326-2

|

PLT & MACH RENT & SERV

|

E

|

|

326-28

|

Oth Plt & Mach Services

|

E

|

|

326-29

|

Oth Plt & Mach Rental

|

E

|

|

326-4

|

MOTOR VEHICLE RENTAL

|

E

|

|

326-41

|

Forklift Rental

|

E

|

|

326-49

|

Motor Vehicle Rental

|

E

|

|

327-

|

HEALTH & SAFETY

|

E

|

|

327-0

|

Clinic Fees

|

E

|

|

327-1

|

P O1160

|

E

|

|

327-2

|

Certification Costs

|

E

|

|

327-3

|

Stack & Dust Monitoring

|

E

|

|

327-4

|

Fire Equipment

|

E

|

|

327-5

|

Hygiene Surveys

|

E

|

|

327-6

|

Health Professional Fees

|

E

|

|

327-7

|

Medication

|

E

|

|

327-8

|

Ext Medical Screening

|

E

|

|

327-9

|

Other Health & Safety

|

E

|

|

328-

|

INSURANCE

|

E

|

|

328-1

|

Asset Value Insurance

|

E

|

|

329-

|

SUNDRY FIXED FACTORY OH

|

E

|

|

329-0

|

TOOLING REPLACE PROVISION

|

E

|

|

329-1

|

Tooling Replace Prov

|

E

|

|

329-1

|

TOOLING AMORTIZATION

|

E

|

|

329-11

|

Tooling Amortization

|

E

|

|

329-2

|

DEVELOPMENT EXPENSES

|

E

|

|

329-21

|

Trial Costs

|

E

|

|

329-23

|

R & D Costs

|

E

|

|

329-25

|

Project Costs

|

E

|

|

329-28

|

Magmasoft Costs

|

E

|

|

329-29

|

Other Development Costs

|

E

|

|

329-3

|

TRAINING

|

E

|

|

329-31

|

Apprentice Training

|

E

|

|

329-33

|

Trg Course Fees Sal

|

E

|

|

329-34

|

Trg Course Fees Wage

|

E

|

|

329-35

|

Train Trav & Accom Sal

|

E

|

|

329-36

|

Train Trav & Accom Wag

|

E

|

|

329-39

|

Training Other

|

E

|

|

329-4

|

CONSULTING FEES

|

E

|

|

329-41

|

Consulting Fee Factory

|

E

|

|

329-45

|

Consulting Fee Quality

|

E

|

|

329-47

|

Consulting Fee Division5

|

E

|

|

329-49

|

Consulting Fee Other

|

E

|

|

329-5

|

COMPUTER EXP PLANT

|

E

|

|

329-51

|

Software Costs Plant

|

E

|

|

329-52

|

Softw Licence Plant

|

E

|

|

329-53

|

Hardware Under R5000

|

E

|

|

329-54

|

IT Prof Serv Plant

|

E

|

|

329-55

|

Prod Report Improve

|

E

|

|

329-56

|

Computer Maint Plant

|

E

|

|

329-59

|

Other Computer Exp Plant

|

E

|

|

329-6

|

LEASE CHARGES (LCh)

|

E

|

|

329-62

|

PLANT & MACHINERY LCh

|

E

|

|

329-621

|

Plant & Machinery LCh

|

E

|

|

329-64

|

MOTOR VEHICLES LCh

|

E

|

|

329-641

|

Forklifts LCh

|

E

|

|

329-649

|

Other Motor Veh LCh

|

E

|

|

329-65

|

OFFICE EQUIPMENT LCh

|

E

|

|

329-651

|

Office Equipment LCh

|

E

|

|

329-66

|

COMPUTERS LCh

|

E

|

|

329-661

|

Computers LCh

|

E

|

|

329-67

|

FURNITURE & FITTINGS LCh

|

E

|

|

329-671

|

Furniture & Fit LCh

|

E

|

|

329-7

|

SECURITY

|

E

|

|

329-71

|

Security

|

E

|

|

329-8

|

PROPERTY RENTAL

|

E

|

|

329-81

|

Property Rental Ext

|

E

|

|

329-82

|

Property Rental Int

|

E

|

|

329-9

|

RATES & TAXES

|

E

|

|

329-91

|

Rates & Taxes

|

E

|

|

329-W

|

OTHER STAFF FIXED

|

E

|

|

329-W1

|

Workmens Comp Paid Fix

|

E

|

|

329-W3

|

Staff Welfare Fixed

|

E

|

|

329-W5

|

Staff Transport Fixed

|

E

|

|

329-Z

|

OTHER FIXED

|

E

|

|

329-Z1

|

Cleaning Contract

|

E

|

|

329-Z3

|

Printing & Stationery Fix

|

E

|

|

329-Z9

|

Other Fixed

|

E

|

|

32A-

|

IMPAIRMENT FIX ASSETS (IFA)

|

E

|

|

32A-0

|

Land IFA

|

E

|

|

32A-1

|

Buildings IFA

|

E

|

|

32A-2

|

Plant & Machinery IFA

|

E

|

|

32A-4

|

Motor Vehicles IFA

|

E

|

|

32A-5

|

Office Equipment IFA

|

E

|

|

32A-6

|

Computers IFA

|

E

|

|

32A-7

|

Furniture & Fittings IFA

|

E

|

|

32A-8

|

Intangible Assets IFA

|

E

|

|

32B-

|

CANTEEN COSTS

|

E

|

|

32B-0

|

Canteen Costs

|

E

|

|

32B-3

|

Canteen Consumables

|

E

|

|

32B-9

|

Other Catering Costs

|

E

|

|

33.-

|

VARIABLE FACTORY OVERHEADS

|

E

|

|

331-

|

SCRAP COSTS

|

E

|

|

331-1

|

Casting Scrap

|

E

|

|

331-3

|

Core Scrap

|

E

|

|

331-4

|

External Casting Scrap

|

E

|

|

331-5

|

Machining Scrap

|

E

|

|

331-6

|

Trial Scrap

|

E

|

|

331-7

|

External Scrap Machine Shop

|

E

|

|

331-8

|

External Scrap Customer Ret

|

E

|

|

331-9

|

Other Scrap Internal

|

E

|

|

332-

|

ENERGY & UTILITIES

|

E

|

|

332-1

|

Electricity -- KWH

|

E

|

|

332-2

|

Gas

|

E

|

|

332-5

|

Diesel

|

E

|

|

332-9

|

Water & Effluent

|

E

|

|

333-

|

VARIABLE REP & MAINT (R&M)

|

E

|

|

333-1

|

BUILDING R&M

|

E

|

|

333-11

|

Building R&M

|

E

|

|

333-2

|

PLANT & MACHINERY R&M

|

E

|

|

333-21

|

Reline Costs

|

E

|

|

333-22

|

Pattern R&M

|

E

|

|

333-23

|

Var Electrical R&M

|

E

|

|

333-24

|

Var Mechanical R&M

|

E

|

|

333-25

|

Var Shutdown Elect R&M

|

E

|

|

333-26

|

Var Shutdown Mech R&M

|

E

|

|

333-27

|

Var Fact Improve Elect

|

E

|

|

333-28

|

Var Fact Improve Mech

|

E

|

|

333-29

|

Oth Plt & Machinery R&M

|

E

|

|

333-3

|

TOOLING R&M

|

E

|

|

333-30

|

Core Making Tooling R&M

|

E

|

|

333-31

|

Pattern / Dies Tooling R&M

|

E

|

|

333-32

|

Moulding Box Repairs

|

E

|

|

333-33

|

Dry Ice

|

E

|

|

333-34

|

Glass Beads

|

E

|

|

333-35

|

Other Tooling R&M

|

E

|

|

333-4

|

MOTOR VEHICLES R&M

|

E

|

|

333-41

|

Forklifts R&M

|

E

|

|

333-49

|

Oth Motor Vehicles R&M

|

E

|

|

333-5

|

OFFICE EQUIPMENT R&M

|

E

|

|

333-51

|

Office Equipment R&M

|

E

|

|

333-6

|

COMPUTER R&M

|

E

|

|

333-61

|

Computer R&M

|

E

|

|

333-7

|

FURNITURE & FITTINGS R&M

|

E

|

|

333-71

|

Furniture & Fitt R&M

|

E

|

|

334-

|

CONSUMABLES

|

E

|

|

334-2

|

FOUNDRY CONSUMABLES

|

E

|

|

334-21

|

Alloying Consumables

|

E

|

|

334-22

|

Melting Consumables

|

E

|

|

334-221

|

Slag Coagulant

|

E

|

|

334-222

|

Thermocouples Melt

|

E

|

|

334-223

|

Crucibles

|

E

|

|

334-228

|

Oth Melt Consumables A

|

E

|

|

334-229

|

Oth Melt Consumables B

|

E

|

|

334-24

|

Sand Plant Consumables

|

E

|

|

334-26

|

Core Making Consumables

|

E

|

|

334-28

|

Moulding Consumables

|

E

|

|

334-281

|

Moulding Consumables

|

E

|

|

334-282

|

Thermocouples Mould

|

E

|

|

334-289

|

Oth Mould Consumables

|

E

|

|

334-29

|

Oth Foundry Consumables

|

E

|

|

334-3

|

FINISHING CONSUMABLES

|

E

|

|

334-31

|

Finishing Consumables

|

E

|

|

334-311

|

Grinding Consumables

|

E

|

|

334-319

|

Oth Finish Consmbls

|

E

|

|

334-33

|

Painting Consumables

|

E

|

|

334-35

|

Heat Treat Consumables

|

E

|

|

334-37

|

Impregnatn Consumables

|

E

|

|

334-38

|

Welding Consumables

|

E

|

|

334-39

|

Oth Finishing Consumbls

|

E

|

|

334-4

|

MACHINE & ASSEMBLY CONS

|

E

|

|

334-41

|

Machining Consumables

|

E

|

|

334-411

|

Mach Cons Customer11

|

E

|

|

334-412

|

Oils & Lubricants

|

E

|

|

334-419

|

Oth Machining Consbls

|

E

|

|

334-43

|

Sub-Assembly Consbls

|

E

|

|

334-45

|

Final Assembly Consbls

|

E

|

|

334-49

|

Oth Mach & Ass Coins

|

E

|

|

334-6

|

OPERATIONAL CONSUMABLES

|

E

|

|

334-60

|

Maintenance Consumables

|

E

|

|

334-61

|

Laboratory Consumables

|

E

|

|

334-62

|

Insp Metr & QC Cons

|

E

|

|

334-63

|

Pattern Shop Consmbls

|

E

|

|

334-64

|

Sand Reclamation Cons

|

E

|

|

334-65

|

Stores Consumables

|

E

|

|

334-66

|

Logistics & Disp Cons

|

E

|

|

334-67

|

Development Consumables

|

E

|

|

334-68

|

Process Eng Consumables

|

E

|

|

334-69

|

Safety Sec Clean Cons

|

E

|

|

334-6Z

|

Oth Op Consumables

|

E

|

|

334-7

|

VEHICLE EXPENSES

|

E

|

|

334-70

|

Vehicle Licenses

|

E

|

|

334-71

|

Vehicle Fines & Penalties

|

E

|

|

334-72

|

Vehicle Fuel

|

E

|

|

334-74

|

Vehicle Op Rental

|

E

|

|

334-79

|

Other Vehicle Expenses

|

E

|

|

334-9

|

OTHER CONSUMABLES

|

E

|

|

334-90

|

Gauges

|

E

|

|

334-91

|

Small Tools (Durable)

|

E

|

|

334-92

|

Durable Machine Tools

|

E

|

|

334-93

|

Non Durable Machine Tools

|

E

|

|

334-94

|

Consumable Tooling

|

E

|

|

334-95

|

Hand Tools

|

E

|

|

334-96

|

Gases

|

E

|

|

334-961

|

Liquid Nitrogen

|

E

|

|

334-969

|

Other Gases

|

E

|

|

334-97

|

Cutting Tools

|

E

|

|

334-98

|

Printing & Stationery

|

E

|

|

334-99

|

Other Consumables

|

E

|

|

335-

|

TRANSPORT & PACKING

|

E

|

|

335-1

|

Packaging Materials

|

E

|

|

335-11

|

Crate Hire

|

E

|

|

335-15

|

Other Packaging

|

E

|

|

335-2

|

FOB Costs

|

E

|

|

335-3

|

Maritime Insurance

|

E

|

|

335-4

|

Freight Costs (Sea)

|

E

|

|

335-5

|

DAP Costs

|

E

|

|

335-6

|

Airfreight

|

E

|

|

335-7

|

Railage & Road Freight

|

E

|

|

335-71

|

Rail & Road Inbound

|

E

|

|

335-75

|

Rail & Road Outbound

|

E

|

|

335-9

|

Other Transport

|

E

|

|

336-

|

WASTE REMOVAL & CLEANING

|

E

|

|

336-1

|

Sand Waste Removal

|

E

|

|

336-3

|

Sand Reclamation Costs

|

E

|

|

336-4

|

General Waste Removal

|

E

|

|

336-5

|

Cleaning Costs

|

E

|

|

336-6

|

Sorting Costs

|

E

|

|

338-

|

Division5 LABOUR RECOVERY

|

E

|

|

338-1

|

Division5 Labour Recovery

|

E

|

|

339-

|

OTHER VARIABLE COSTS

|

E

|

|

339-1

|

PPE Variable Cost

|

E

|

|

339-3

|

Subcontractor Machining

|

E

|

|

339-4

|

Staff Transport

|

E

|

|

339-5

|

Rework

|

E

|

|

339-6

|

Regrinding of Tools

|

E

|

|

339-7

|

Stripping Costs

|

E

|

|

339-8

|

Staff Welfare

|

E

|

|

339-9

|

Other Variable Costs

|

E

|

|

34.-

|

ADMIN EXPENSES

|

E

|

|

340-

|

ADMIN STAFF COSTS

|

E

|

|

340-1

|

ADMIN SALARIES

|

E

|

|

340-10

|

Normal Time Adm Sal

|

E

|

|

340-11

|

Overtime Adm Sal

|

E

|

|

340-12

|

Allowances Adm Sal

|

E

|

|

340-13

|

Bonus Long Serv Adm Sal

|

E

|

|

340-15

|

Company Contrib Adm Sal

|

E

|

|

340-18

|

Retrench Costs Adm Sal

|

E

|

|

340-3

|

DIRECTORS REMUNERATION

|

E

|

|

340-31

|

EXECUTIVE DIR REM

|

E

|

|

340-311

|

Basic Sal Exec Dir Rm

|